When prices at the grocery store, gas station, and on your utility bills keep climbing, most Americans ask the same question: How do I protect what I’ve saved? Inflation quietly eats away at your purchasing power, making every dollar worth a little less over time. That’s why millions of investors, retirees, and savers turn their attention to gold.

Understanding how gold performs during inflation is crucial if you’re serious about preserving your wealth. Gold has been a trusted store of value for thousands of years, long before the U.S. dollar even existed. In today’s financial markets, it still holds a unique spot: part insurance policy, part investment, and a psychological comfort when the economy gets rocky.

This guide breaks down the connection between gold and inflation in plain English, using real historical data, honest comparisons to other assets, and practical advice for American investors on how to use gold in their portfolios.

Inflation and Your Money

What Inflation Really Means for Your Wallet

Inflation is simply how fast the general price of goods and services goes up over time. If inflation is at 4%, a $100 grocery bill this year becomes $104 next year for the same items. Over a decade, that compounding effect can seriously cut into what your savings can actually buy.

The Federal Reserve usually aims for an inflation rate of around 2% annually, considering it healthy for the economy. But during times of economic upheaval—like a pandemic, an energy crisis, or rapid government spending—inflation can jump much higher, sometimes to levels not seen in decades.

Why Inflation Erodes Savings

Here’s the problem with holding cash when inflation is high: banks rarely offer interest rates that beat inflation. When inflation topped 8% in 2022, even high-yield savings accounts were only paying 0.5% to 2%. This meant savers were losing purchasing power every single month.

Bonds and CDs face similar issues. A 10-year Treasury bond locked in at a 2% yield loses real value if inflation runs at 5% or 6% during that time. This is why investors look for inflation-resistant assets—investments whose value tends to rise with or faster than general prices.

Why Investors Seek Inflation Hedges

An inflation hedge is an asset that historically keeps or grows its real value when consumer prices go up. Effective hedges usually have a few things in common:

1. They have inherent value not solely tied to currency.

2. Their supply is limited or hard to increase quickly.

3. They’re widely recognized and trusted as a store of value.

4. They tend to be in demand precisely when confidence in paper money is low.

Gold checks all these boxes, which is why it’s been the go-to inflation hedge for generations.

Why Investors Turn to Gold When Inflation Starts Rising

Gold’s Historical Role in Money

Gold’s connection to money isn’t new. For most of human history, currencies were literally backed by gold or silver. The U.S. was on a formal gold standard until 1971, when President Nixon cut the dollar’s link to gold—an event known as the “Nixon Shock.” From then on, the dollar became a pure fiat currency, backed only by the U.S. government’s full faith and credit.

This change matters because fiat currencies can theoretically be created in unlimited amounts. When governments and central banks rapidly expand the money supply, each unit of currency tends to buy less. Gold, on the other hand, can’t be printed. Its supply only grows by what miners can dig out of the earth—historically about 1% to 3% per year.

Scarcity and Intrinsic Value

One of gold’s most important features is its limited supply. According to the World Gold Council, all the gold ever mined would fill roughly three and a half Olympic swimming pools. That scarcity gives gold an intrinsic value that paper assets just don’t have.

Unlike stocks or bonds, gold doesn’t pay dividends or interest. Its value comes from what people are willing to pay for it, and that demand tends to surge when confidence in the financial system wavers.

Investor Psychology During Inflation

There’s a powerful psychological aspect to gold’s role as an inflation hedge. When inflation rises sharply, investors worry about the long-term stability of fiat currency. Money tends to shift out of interest-bearing assets (whose real returns shrink) and into hard assets like gold, real estate, and commodities.

This self-fulfilling dynamic—people buy gold because others buy gold when they’re scared—is one reason gold can rise sharply during inflationary crises, sometimes far beyond what fundamentals alone would suggest.

Gold’s Historical Performance During Inflation

The 1970s: Gold’s Defining Decade

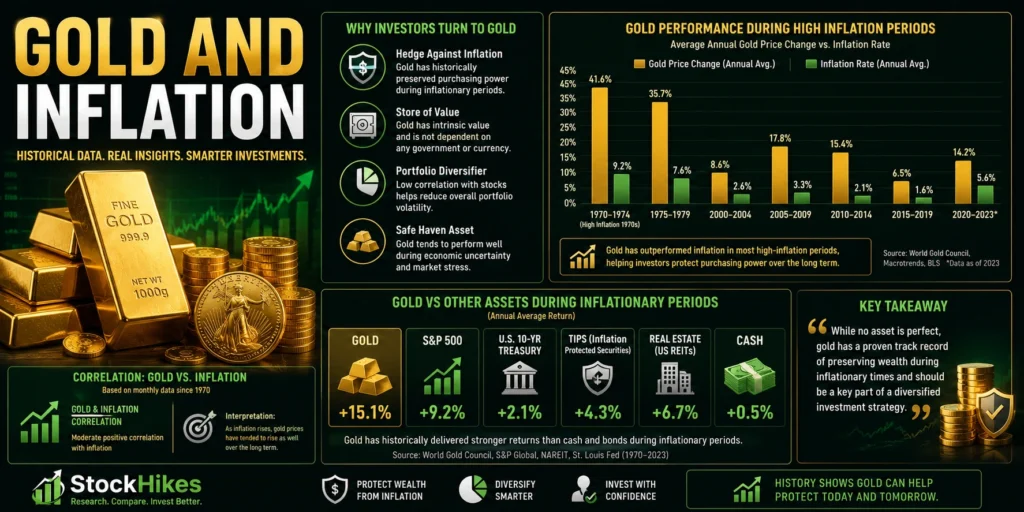

The 1970s remain the classic example (no pun intended) of how gold performs during inflation. After Nixon ended the dollar-gold convertibility in 1971, inflation started creeping up. By the late 1970s, the U.S. was seeing double-digit inflation, peaking at about 14.8% in 1980.

Gold’s reaction was dramatic. In January 1970, gold was around $35 per ounce. By January 1980, it had skyrocketed to about $850 per ounce—a gain of over 2,300% in nominal terms. Even with the high inflation of that decade, the real return was extraordinary.

This period is often cited as proof that gold is an effective inflation hedge, but context matters. Gold’s gains were partly fueled by the structural shock of leaving the gold standard, a one-time event that supercharged demand.

The Early 2000s: Moderate Inflation, Steady Gold Gains

In the early 2000s, inflation was modest, generally between 2% and 4%. Yet, gold still climbed steadily, rising from about $270 per ounce in 2001 to over $1,000 by early 2008.

This rise wasn’t just due to inflation expectations. It was also driven by a weakening U.S. dollar, geopolitical uncertainty after September 11, 2001, and strong demand from emerging markets like India and China. It’s a good reminder that while gold and inflation are linked, it’s rarely the only factor at play.

The Post-Pandemic Inflation Surge (2021–2023)

When COVID-19 relief spending, supply chain issues, and the Russia-Ukraine war pushed U.S. inflation above 9% in June 2022—the highest in 40 years—many investors expected gold to soar.

The reality was more complex. Gold did hit an all-time high of around $2,075 per ounce in August 2020 (due to pandemic uncertainty). But through most of 2021 and into 2022, gold actually underperformed. By late 2022, it had dropped to about $1,625. The reason? The Federal Reserve aggressively raised interest rates to fight inflation, which boosted real yields and made interest-bearing assets more attractive compared to gold.

Gold eventually recovered and set new records, topping $2,400 per ounce in mid-2024, as inflation started to cool and expectations for rate cuts grew.

| Period | Inflation Level | Gold’s Performance | Key Drivers |

| 1970s | 7–14% | +2,300% nominal | Dollar devaluation, geopolitical crisis |

| Early 2000s | 2–4% | +270% over decade | Weak dollar, war, EM demand |

| 2008–2012 | 0–4% | Rose from ~$800 to $1,900 | Financial crisis, QE fears |

| 2020–2022 | 5–9% | Mixed — peaked then fell | Rate hike expectations overshadowed inflation |

| 2023–2024 | 3–5% | New all-time highs | Rate pause hopes, central bank buying |

| 2025–2026 | 2.6–3.8% | +55% in 2025; new ATH of ~$3,500+ (Apr 2025), then ~$5,500+ (Jan 2026) | Tariff uncertainty, Iran war oil shock, weak dollar, record central bank buying, safe-haven demand |

When Gold Shines During Inflation

Understanding the conditions under which gold performs best is more helpful than just knowing it can be an inflation hedge.

High Inflation Environments

When inflation is significantly above the Fed’s 2% target—especially in the 5%, 8%, or double-digit range—gold tends to attract more capital. In these situations, real returns on bonds often become negative, essentially eliminating the opportunity cost of holding gold (which pays no interest).

Currency Weakness

Gold is priced globally in U.S. dollars. When the dollar weakens, it takes more dollars to buy the same ounce of gold, meaning gold prices rise in dollar terms. Periods of dollar weakness often coincide with high inflation and tend to amplify gold’s gains.

Economic Uncertainty and Geopolitical Risk

Gold is often called a “safe haven asset” because investors flock to it during crises—financial panics, wars, banking failures, and recessions. This flight-to-safety demand can push gold higher even when inflation isn’t the main driver.

Central Bank Policy Shifts

When the Federal Reserve indicates it will slow or stop interest rate hikes, or start cutting rates, real yields typically fall. This environment is historically good for gold. Central bank buying from other nations (China, India, Poland, and others have been major buyers recently) also provides a significant floor for demand.

When Gold Might Not Be Your Best Bet

A fair assessment of gold means acknowledging its limitations. Gold isn’t a guaranteed hedge against every inflationary scenario.

Rising Real Interest Rates

This is gold’s biggest challenge. When the Federal Reserve aggressively raises rates to fight inflation—as it did in 2022—real yields (the interest rate minus inflation) can climb sharply. At that point, Treasury bonds and other interest-bearing investments become more appealing than gold, which offers no yield.

Strong U.S. Dollar Periods

A strong dollar usually puts pressure on gold prices. When U.S. economic data outperforms the rest of the world, capital flows into dollar-denominated assets, strengthening the currency and weighing on commodities priced in dollars.

Short-Term Volatility

Gold can be very volatile in the short term. Investors who buy at market peaks expecting immediate protection can face painful drops. In 2011, gold hit nearly $1,900 per ounce before plummeting to around $1,050 by 2015—a 45% decline. It didn’t regain that 2011 high until 2020.

Mild Inflation Environments

When inflation is modest—around 2% to 3%—and the economy is growing steadily, stocks and real estate often do better than gold. Gold tends to lag in healthy, low-volatility economic times.

Gold vs. Other Inflation Hedges

Gold isn’t the only tool for inflation protection. Here’s how it stacks up against other common options.

Gold vs. Stocks

Stocks have historically outperformed gold over long, multi-decade periods. The S&P 500’s average annual return of roughly 10% (nominal) since 1928 far exceeds gold’s long-term average. However, stocks can suffer greatly during stagflation (high inflation + slow growth), as they did in the 1970s. Many companies also struggle to pass rising costs on to consumers. Gold tends to be a better short-term inflation shock absorber, while stocks win over the long haul.

Gold vs. Real Estate

Real estate has strong inflation-hedging qualities because property values and rents tend to rise with inflation. Real estate also provides income, which gold doesn’t. The downside is that real estate is illiquid, requires a lot of capital, and comes with management costs. Gold is much easier to buy and sell quickly.

Gold vs. TIPS (Treasury Inflation-Protected Securities)

TIPS are U.S. government bonds specifically designed to protect against inflation—their principal adjusts with the Consumer Price Index. They’re lower-risk than gold and pay interest. The drawback is that TIPS returns are tied to official CPI measurements, while gold can react to expectations of inflation before CPI data confirms it. In severe inflation scenarios, gold has historically outperformed TIPS.

Gold vs. Cash Savings

Cash in savings accounts is one of the worst inflation hedges. During high-inflation periods, the real purchasing power of cash steadily erodes. Even high-yield accounts rarely keep pace with surging prices. Gold, despite its volatility, has maintained real purchasing power over centuries in ways that paper currency simply hasn’t.

| Asset | Inflation Hedge? | Income? | Liquidity | Volatility |

| Gold | Strong (long-term) | No | High | Medium-High |

| Stocks | Moderate | Yes (dividends) | High | High |

| Real Estate | Strong | Yes (rent) | Low | Low-Medium |

| TIPS | Strong (measured) | Yes (interest) | Medium | Low |

| Cash/Savings | Very Weak | Yes (interest) | Highest | Very Low |

Ways Americans Can Invest in Gold

There are several practical ways to add gold to your portfolio, each with different pros and cons.

Physical Gold (Coins and Bars)

Buying gold coins (like American Gold Eagles or Canadian Maple Leafs) or bars gives you direct ownership of the metal. This is the most tangible way to own gold.

Pros: No counterparty risk, direct ownership, portable.

Cons: Storage and insurance costs, dealer premiums above spot price, less liquid than ETFs.

Gold ETFs (Exchange-Traded Funds)

Funds like SPDR Gold Shares (GLD) and iShares Gold Trust (IAU) hold physical gold and trade on stock exchanges just like any stock. They’re a popular and convenient way to get gold exposure.

Pros: Low cost, highly liquid, no storage hassle.

Cons: Management fees, no physical gold in hand, may not track spot gold prices perfectly.

Gold Mining Stocks

Companies like Newmont, Barrick Gold, and Agnico Eagle mine gold and can offer leveraged exposure to gold prices. When gold rises, mining companies’ profits often increase even faster (and fall faster when gold drops).

Pros: Potential for dividends, leveraged upside, can outperform gold itself.

Cons: Company-specific risks (management, mine production, costs), higher volatility than gold itself.

Gold Mutual Funds

Some mutual funds invest in a diversified mix of gold mining stocks and might hold some physical gold. These offer diversification across mining companies and professional management.

Pros: Diversification across mining companies, professional management.

Cons: Higher fees than ETFs, subject to the same mining company risks.

Gold IRAs

A Gold IRA is a self-directed individual retirement account that holds physical precious metals. This can be a tax-advantaged way to add gold to your retirement savings.

Pros: Tax advantages of an IRA, physical gold ownership.

Cons: Higher fees (custodian, storage), strict IRS rules on eligible metals, limited liquidity.

Common Mistakes Investors Make With Gold

Over-allocating to Gold

Gold doesn’t pay dividends, interest, or rent. Putting too much of your portfolio into gold (say, 30–40%) means giving up significant income-generating potential. Most financial professionals suggest keeping gold as a modest part of a diversified portfolio.

Buying During Market Panic

The worst time to buy most assets—including gold—is at the peak of a fear-driven rally. When headlines are screaming about economic collapse, gold prices are often already inflated. Disciplined, regular purchases usually work better than reactive panic buying.

Ignoring Diversification

Gold is an addition to a portfolio, not a replacement for a diversified investment strategy. Investors who sell all their stocks and bonds to buy gold are taking on a different kind of risk—one that has underperformed equities over most long-term periods.

Underestimating Costs

Physical gold comes with dealer premiums, storage fees, and insurance. Gold IRAs can have custodian fees and account minimums. Even gold ETFs have management expense ratios. Over time, these costs can significantly reduce your net returns, especially if gold prices are flat or falling.

How Much Gold Should Be in Your Portfolio?

Financial professionals and economists offer different advice on gold allocation, but some common themes emerge.

Most mainstream financial advisors suggest a 5% to 10% allocation to gold or precious metals for a typical portfolio. This provides meaningful inflation protection and reduces overall portfolio volatility without sacrificing too much return potential.

More conservative investors or retirees with high inflation concerns might hold 10% to 15% in gold-related assets. Those with a higher risk tolerance who strongly believe in precious metals might go higher, though allocations above 20% are generally considered concentrated.

The right allocation also depends on:

- Time horizon: Longer-term investors can afford to ride out gold’s volatility.

- Existing inflation protection: If you already own real estate or TIPS, you might need less gold.

- Income needs: Retirees relying on portfolio income might prefer dividend-paying assets over gold.

There’s no single right answer. Gold’s role in a portfolio is personal and should be discussed with a qualified financial advisor based on your individual circumstances.

Who Should Consider Gold?

Gold isn’t a necessity for every investor, but it can play a valuable role in certain financial situations. Understanding whether gold fits your goals is often more important than trying to predict its next price move.

Retirees Concerned About Inflation

Retirees are often among the biggest supporters of gold because inflation can gradually reduce the purchasing power of fixed retirement income. While gold doesn’t generate income like dividend stocks or bonds, it can help preserve wealth during periods of rising prices and economic uncertainty. A modest allocation may provide an additional layer of protection for retirement savings.

Investors Approaching Retirement

People within five to ten years of retirement often become more focused on preserving capital than maximizing growth. Since gold tends to behave differently from stocks and bonds, it can help diversify a portfolio and potentially reduce overall volatility during turbulent market conditions.

Investors Seeking Diversification

Many investors hold gold not because they expect it to outperform every other asset, but because it often moves independently of traditional investments. Adding a small allocation to gold can help balance a portfolio that is heavily concentrated in stocks, bonds, or real estate.

Those Concerned About Economic or Geopolitical Uncertainty

Periods of high inflation, banking stress, geopolitical conflicts, or concerns about government debt often increase interest in gold. Investors who want exposure to an asset that has historically served as a store of value during uncertain times may find gold appealing as part of a broader risk-management strategy.

Gold IRA Investors

Some retirement savers choose to hold physical precious metals through a self-directed Gold IRA. While Gold IRAs involve additional costs and regulations, they may appeal to investors who prefer direct ownership of precious metals within a tax-advantaged retirement account.

Related Reading: Gold IRA Fees Explained: Complete Cost Breakdown for Investors

Who May Need Less Gold?

Investors with long-term horizons, strong risk tolerance, and a primary focus on growth may not need a large gold allocation. Historically, diversified stock portfolios have delivered higher long-term returns than gold. For these investors, gold may serve as a modest portfolio stabilizer rather than a major investment position.

Ultimately, gold is not a one-size-fits-all solution. The right allocation depends on your financial goals, risk tolerance, time horizon, and overall investment strategy. For most investors, gold works best as a complement to a diversified portfolio rather than a replacement for traditional growth and income-producing assets.

Expert Insights and Economic Perspectives

The debate about gold’s place in modern portfolios is lively among economists and wealth managers.

The bull case: Advocates like Ray Dalio see gold as a critical hedge against currency debasement and debt-driven monetary expansion. Dalio has long argued that in a world of rising debt and aggressive money creation, traditional cash and bonds face structural challenges that can make gold a valuable portfolio diversifier. He has even remarked that “if you don’t own gold, you know neither history nor economics,” highlighting his belief that investors should understand gold’s historical role in preserving wealth during periods of monetary uncertainty.

The skeptical view: Nobel Prize-winning economist Paul Samuelson famously called gold a “barbarous relic” with little place in a modern portfolio. Warren Buffett has long been critical of gold, noting that it doesn’t produce anything—unlike a business or a farm—and that its returns over the past century have dramatically underperformed equities.

Academic research perspective: A widely cited study by researchers Claude Erb and Campbell Harvey found that gold’s ability to hedge inflation is much stronger over very long periods (decades) than over shorter horizons of a few years. They concluded that gold maintains purchasing power over centuries but can badly underperform inflation over periods of 5 to 10 years.

Central bank behavior: Central banks worldwide—including those of China, India, Poland, and Turkey—have been aggressively buying gold recently, reaching record levels of purchases in 2022 and 2023. This institutional demand reflects a broader global trend of reducing reliance on the U.S. dollar as the sole reserve currency.

The takeaway from professional perspectives is nuanced: gold can be a valuable portfolio tool, but it works best as part of a balanced, long-term strategy rather than as a speculative bet or an all-or-nothing trade.

Frequently Asked Questions (FAQ)

Does gold always go up during inflation?

No. Gold doesn’t automatically rise every time inflation increases. Its performance during inflationary periods depends heavily on real interest rates, the U.S. dollar’s direction, and overall investor sentiment. For example, during the 2022 inflationary surge, gold actually declined for much of the year as the Federal Reserve aggressively raised interest rates. Over very long periods, gold has maintained its real purchasing power, but short-term performance can differ significantly from inflation trends.

Why did gold fall in 2022 when inflation was so high?

In 2022, the Federal Reserve raised interest rates at the fastest pace in decades to combat inflation above 8%. Higher interest rates increased the yield on Treasury bonds and other safe assets, making gold (which pays no yield) relatively less attractive. Real interest rates turned positive for the first time in years, which historically puts pressure on gold prices. This shows why gold’s relationship with inflation isn’t always straightforward.

Is gold a better inflation hedge than stocks?

Over short to medium-term inflationary periods, gold has historically offered stronger protection than stocks—especially when inflation is high and economic growth is sluggish (stagflation). Over longer periods spanning multiple decades, stocks have significantly outperformed gold in total return. Most financial professionals recommend holding both as part of a diversified strategy rather than choosing one over the other.

How much of my portfolio should be in gold?

Most financial professionals suggest a modest allocation of 5% to 10% of a portfolio in gold or precious metals. This provides meaningful inflation protection without sacrificing the income and growth potential of equities and bonds. The right amount depends on your specific financial situation, time horizon, and risk tolerance. It’s worth discussing with a fiduciary financial advisor.

What’s the safest way to invest in gold?

For most Americans, a gold ETF like GLD (SPDR Gold Shares) or IAU (iShares Gold Trust) is considered the most practical, low-cost way to get gold exposure. These ETFs are backed by physical gold held in vaults and trade like stocks on major exchanges. Physical gold (coins or bars) is suitable for those who want direct ownership but requires attention to storage and insurance costs. Gold IRAs can be advantageous for retirement savers but come with higher fees and IRS regulations.

Is physical gold better than gold ETFs?

It depends on your priorities. Physical gold eliminates counterparty risk (no financial institution can default on metal you personally own), but it requires secure storage and comes with dealer premiums. Gold ETFs are more convenient, liquid, and cost-effective for most investors. Some people hold a combination—a core ETF position for liquidity and a small amount of physical gold for direct ownership.

What happens to gold during a recession?

Gold’s performance during recessions varies. If a recession is accompanied by deflation (falling prices), gold may underperform. If a recession involves inflation (stagflation) or significant monetary stimulus (like quantitative easing), gold tends to perform well. During the 2008 financial crisis, gold initially sold off as investors needed liquidity, then surged strongly as the Fed implemented emergency stimulus measures.

Does the U.S. dollar’s strength affect gold prices?

Yes, significantly. Since gold is priced in U.S. dollars globally, a strong dollar makes gold more expensive for foreign buyers and tends to suppress prices. A weak dollar has the opposite effect—it tends to support and push gold prices higher. Monitoring the U.S. Dollar Index (DXY) alongside gold prices gives investors a clearer picture of what’s driving gold’s movements.

Is gold a good investment for retirement?

Gold can play a role in retirement planning as a portfolio stabilizer and inflation hedge, but it should rarely be the main focus of a retirement strategy. Retirees typically need income-generating assets (dividends, bond interest, rental income), which gold doesn’t provide. A modest gold allocation (5%–10%) within a diversified retirement portfolio can reduce volatility and offer protection against inflationary shocks—but it works best as a component, not a foundation.

What factors cause gold prices to rise?

Multiple factors drive gold prices higher, including rising inflation expectations, falling real interest rates, U.S. dollar weakness, geopolitical crises or economic uncertainty, central bank buying, increased investor demand for safe haven assets, and supply constraints in mining. Gold rarely moves on a single factor alone—it typically responds to a combination of these dynamics happening simultaneously.

Final Verdict: What Investors Should Know About Gold and Inflation

Gold has earned its reputation as a store of value, but its relationship with inflation is more nuanced than many investors realize. While it has historically helped preserve purchasing power over long periods and often performs well during times of economic uncertainty, inflation alone does not guarantee rising gold prices. Factors such as interest rates, U.S. dollar strength, investor sentiment, and central bank policies can all have a significant impact on gold’s performance.

For most investors, gold works best as a supporting player rather than the centerpiece of a portfolio. It can provide diversification, help reduce overall portfolio volatility, and offer a measure of protection when inflation is high or confidence in financial markets weakens. However, gold also comes with limitations. It does not generate income, can experience periods of significant price volatility, and has historically underperformed stocks over very long investment horizons.

The key is to view gold for what it is: a long-term risk-management tool rather than a guaranteed path to higher returns. Investors who maintain realistic expectations and use gold as part of a diversified investment strategy are generally better positioned than those who rely on it as a standalone solution.

Practical Investor Takeaway

If you’re considering gold as part of your inflation-protection strategy, a measured approach is usually the most effective. Many financial professionals suggest allocating around 5% to 10% of a diversified portfolio to gold or precious metals. This level of exposure can provide meaningful diversification benefits without sacrificing too much growth potential.

For most Americans, low-cost gold ETFs such as GLD or IAU offer a simple and convenient way to gain exposure to gold without the storage and insurance challenges associated with physical bullion. Whatever approach you choose, avoid making decisions based solely on market headlines or short-term price movements. Gold tends to deliver the greatest value when it’s already part of your portfolio before periods of inflation, market stress, or economic uncertainty arise.

As with any investment decision, consider your financial goals, risk tolerance, and time horizon, and consult a qualified financial advisor if you need personalized guidance.

This article is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. Past performance does not guarantee future results. Always conduct your own research and consult a qualified financial professional before making investment decisions.