Gold has served as a store of value for centuries, but modern investors now have more than one way to own it. Some prefer holding gold coins and bars directly, while others choose to keep precious metals inside a retirement account. As a result, the debate around Gold IRA vs Physical Gold has become increasingly important for people focused on retirement security and long-term wealth preservation.

In recent years, concerns about inflation, market volatility, and growing government debt have encouraged many Americans to look beyond traditional stocks and bonds. Gold is often viewed as a hedge against uncertainty, but the way you own gold can significantly impact taxes, liquidity, storage costs, and overall investment flexibility.

The truth is that neither option is automatically better for everyone. The right choice depends on your financial goals, retirement timeline, risk tolerance, and how much control you want over your assets. This guide examines Gold IRA vs Physical Gold from a practical investor’s perspective so you can determine which approach best fits your long-term strategy.

What Is a Gold IRA?

A Gold IRA is a self-directed individual retirement account that holds physical precious metals instead of — or alongside — traditional paper assets like stocks and bonds. It functions like a standard IRA in terms of tax treatment, but instead of holding mutual funds or ETFs, it holds government-approved gold, silver, platinum, or palladium.

How It Works

You open a Gold IRA through a specialized custodian — a financial institution approved by the IRS to manage self-directed retirement accounts. You then fund the account either through a rollover from an existing 401(k) or traditional IRA, or through direct contributions.

Once funded, you direct the custodian to purchase IRS-approved precious metals on your behalf. The metals are then sent directly to an approved depository, where they’re stored in your name.

IRS-Approved Precious Metals

Not just any gold bar or coin qualifies for a Gold IRA. The IRS has specific purity requirements:

- Gold: Must be at least .995 fine (99.5% pure). Examples include American Gold Eagle coins, Canadian Gold Maple Leafs, and most standard gold bars from approved refiners.

- Silver: Must be at least .999 fine.

- Platinum and Palladium: Must be at least .9995 fine.

Collectible coins, rare coins, and jewelry do not qualify — even if they’re made of gold.

Custodian Requirements

You cannot hold a Gold IRA on your own. The IRS requires a qualified custodian to administer the account. The custodian handles the paperwork, transactions, and annual reporting. They do not give you investment advice, but they do ensure your account stays compliant with IRS rules.

Tax Advantages

A Gold IRA offers the same tax benefits as a standard IRA:

- Traditional Gold IRA: Contributions may be tax-deductible. The gold grows tax-deferred, meaning you won’t owe taxes until you take distributions in retirement.

- Roth Gold IRA: Contributions are made with after-tax dollars, but qualified distributions in retirement are completely tax-free.

This tax-advantaged growth is one of the main reasons investors favor the Gold IRA route for retirement savings.

Storage Requirements

The IRS strictly prohibits Gold IRA holders from keeping their metals at home or in a personal safe. All Gold IRA assets must be stored at an IRS-approved depository. These are highly secure, insured facilities that provide segregated or commingled storage options. Segregated storage means your metals are stored separately and labeled as yours specifically.

What Is Physical Gold?

Physical gold simply means gold you own directly and can hold in your hands. Unlike a Gold IRA, there’s no custodian, no retirement account structure, and no IRS-mandated storage rules. You buy it, and you own it outright.

Gold Coins

Gold coins are the most popular form of physical gold for individual investors. Common options include:

- American Gold Eagle: Produced by the U.S. Mint, available in 1 oz, 1/2 oz, 1/4 oz, and 1/10 oz denominations.

- American Gold Buffalo: A 24-karat (99.99% pure) coin also from the U.S. Mint.

- Canadian Gold Maple Leaf: Known for high purity and wide global recognition.

- South African Krugerrand: One of the most widely traded gold coins worldwide.

Coins typically carry a small premium above the gold spot price due to manufacturing and distribution costs.

Gold Bars

Gold bars (also called gold bullion) offer a cost-effective way to own larger quantities of gold. They come in sizes ranging from 1 gram to 400 troy ounces (the standard “good delivery” bar used in wholesale markets). For most individual investors, 1 oz and 10 oz bars are most practical. Bars carry lower premiums per ounce than coins, making them attractive for buyers focused on maximizing gold content per dollar spent.

Home Storage vs. Vault Storage

When you own physical gold, storage is your decision. Common options include:

- Home safe: Offers immediate access and privacy, but comes with risks of theft and limited insurance coverage.

- Bank safe deposit box: More secure than a home safe, but not insured by the FDIC and inaccessible during bank hours or emergencies.

- Private vault or depository: Professional-grade security, insurance, and peace of mind — but involves ongoing fees.

Direct Ownership Benefits

With physical gold, you are the sole owner. There’s no third party between you and your asset. This appeals to investors who value privacy, simplicity, and the ability to access their gold at any time without going through an institution.

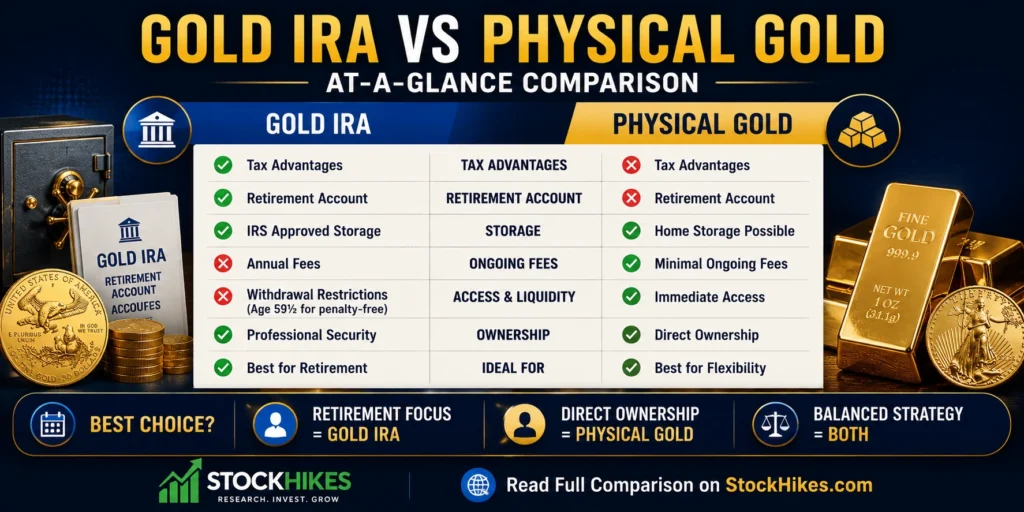

Gold IRA vs Physical Gold: Key Differences

| Feature | Gold IRA | Physical Gold |

|---|---|---|

| Ownership | Held through a custodian in your name | Direct personal ownership |

| Storage | IRS-mandated approved depository | Home, bank, or private vault — your choice |

| Accessibility | Must follow IRA distribution rules; penalties before age 59½ | Accessible at any time, no restrictions |

| Taxes | Tax-deferred (Traditional) or tax-free growth (Roth) | Subject to capital gains tax when sold; collectible rate may apply |

| Liquidity | Must liquidate through custodian; slightly slower process | Can sell to dealers, online platforms, or individuals |

| Security | Professional, insured depository storage | Depends on your storage choice |

| Costs | Setup fees, annual custodian fees, storage fees | Dealer premiums, storage (if vault), insurance |

| Retirement benefits | Strong — tax-advantaged retirement vehicle | None — treated as a capital asset |

| Estate planning | Passes through IRA beneficiary rules | Can be passed directly, may simplify transfer |

| Risk factors | Regulatory changes, custodian risk, distribution penalties | Theft, loss, uninsured storage, emotional decision-making |

Advantages of a Gold IRA

Tax-Deferred or Tax-Free Growth

This is the biggest financial advantage. In a Traditional Gold IRA, your investment grows without being taxed each year. You only pay taxes when you take distributions. If gold appreciates significantly over 20 or 30 years, you’ve compounded that growth without the drag of annual taxes.

In a Roth Gold IRA, you pay taxes upfront and never owe taxes on qualified withdrawals — even if your gold triples in value.

Retirement Diversification

A Gold IRA lets you add gold to your retirement portfolio alongside stocks, bonds, and real estate. Precious metals have historically moved differently from equities, which can reduce overall portfolio volatility during market downturns.

Professional Storage

Your metals are held at a regulated, insured depository. You don’t need to worry about installing a home safe, paying for a bank deposit box, or carrying liability insurance on a physical asset sitting in your home.

Regulatory Oversight

Gold IRAs are governed by IRS rules, which creates a structured framework. While regulations add complexity, they also provide accountability and legal protections that informal physical gold ownership doesn’t offer.

Portfolio Protection in Retirement

Gold has historically served as a hedge against inflation. Including it in a retirement account ensures that a portion of your retirement savings is tied to an asset that tends to hold value when paper currencies decline.

Advantages of Physical Gold

Direct Control

You own the gold. No custodian. No annual reports to file. No waiting on a third party to process a transaction. You can decide exactly when to buy, when to sell, and where to store it.

Immediate Access

Unlike Gold IRA assets — which are subject to early withdrawal penalties if you’re under 59½ — physical gold can be liquidated instantly if you need emergency funds. There are no age restrictions or IRS penalty rules to navigate.

Privacy

Physical gold transactions, especially cash purchases under certain reporting thresholds, offer a degree of privacy that financial accounts do not. There’s no brokerage statement, no 1099, and no account number associated with a bar of gold sitting in a private vault.

No Custodian Involvement

Every layer of institutional involvement adds cost and complexity. Physical gold eliminates the custodian entirely, which means fewer fees and fewer dependencies.

Flexible Purchasing Options

You can buy physical gold from local coin dealers, reputable online bullion dealers, or even pawn shops. The market is accessible to anyone with the funds to purchase, and you can buy in small increments — even a 1/10 oz coin — without minimum investment requirements.

Potential Drawbacks of a Gold IRA

Setup and Annual Fees

Opening a Gold IRA is not free. Expect to pay a one-time setup fee ranging from $50 to $300, depending on the custodian. On top of that, annual administrative fees typically run $75 to $300 per year.

Storage Fees

IRS-approved depositories charge for their services. Storage fees generally range from $100 to $300 per year, though some charge a percentage of the total account value (typically 0.1% to 0.5% annually). Over a 20-year period, these fees can add up to thousands of dollars.

Distribution Rules

You cannot take distributions from a Gold IRA before age 59½ without paying a 10% early withdrawal penalty plus income taxes on the distributed amount. At age 73, the IRS requires you to begin taking Required Minimum Distributions (RMDs), which may force you to sell gold at an inopportune time.

IRS Regulations

Gold IRAs come with strict compliance requirements. The types of metals allowed, where they must be stored, and how distributions must be handled are all governed by IRS rules. Non-compliance can result in penalties, account disqualification, and unexpected taxes.

Potential Drawbacks of Physical Gold

Theft Risk

Gold sitting in a home safe is a target. While good safes provide substantial protection, they don’t eliminate the risk entirely. A theft could cost you your entire physical gold holding with no recourse if it isn’t insured.

Storage Concerns

If you store gold at home, you need a quality safe — which costs money. If you store it in a vault, you pay ongoing fees. Either way, secure storage requires planning and expense.

Insurance Costs

Standard homeowner’s insurance policies typically cover only a few thousand dollars in jewelry or precious metals. Fully insuring a significant gold holding requires a separate rider or a specialized policy, which adds annual costs.

Lack of Tax Advantages

Physical gold doesn’t grow tax-deferred. Every time you sell gold at a profit, the IRS taxes the gain. Gold is classified as a “collectible” by the IRS, meaning long-term capital gains are taxed at a maximum rate of 28% — higher than the 15–20% long-term rate that applies to most stocks.

Emotional Buying Mistakes

When you own physical gold directly, there’s a temptation to make reactive decisions — buying during fear spikes when premiums are high, or selling prematurely during market dips. The institutional structure of a Gold IRA can act as a buffer against impulsive moves.

Cost Comparison

Understanding the true cost of each option helps you compare them fairly.

Gold IRA Costs

- Setup fee: $50–$300 (one-time)

- Annual custodian fee: $75–$300 per year

- Storage fee: $100–$300 per year, or 0.1%–0.5% of account value annually

- Dealer markup: You’ll pay a small premium above spot price when the custodian purchases metals

- Selling fees: Some custodians charge a liquidation fee when you sell

For a $50,000 Gold IRA, you might pay roughly $400–$900 per year in combined fees, totaling around $8,000–$18,000 over 20 years — before accounting for growth.

Physical Gold Costs

- Dealer premium: Coins typically carry 3%–8% above spot price; bars carry 1%–3% above spot

- Shipping costs: Ranges from $25–$50 for insured delivery on standard orders

- Storage: Free (home) to $150–$500 per year (private vault)

- Insurance: $100–$300 per year for meaningful coverage

- Selling: Dealers typically buy back gold at 1%–5% below spot price

For a $50,000 physical gold holding stored in a private vault with insurance, annual ongoing costs might run $300–$800 per year — slightly lower than a Gold IRA, but without the tax advantages.

Tax Considerations

Gold IRA Taxation

- Traditional Gold IRA: Contributions may be deductible. Gains grow tax-deferred. Withdrawals in retirement are taxed as ordinary income.

- Roth Gold IRA: Contributions are not deductible, but qualified withdrawals — including all gains — are tax-free.

- Early withdrawal penalty: 10% penalty for distributions before age 59½, plus ordinary income tax on the distribution amount.

- RMDs: Required Minimum Distributions must begin at age 73. If you prefer to hold your gold long-term, you may be forced to liquidate some of it to meet RMD obligations.

Physical Gold Taxation

- Short-term gains: If you hold gold for less than one year and sell it at a profit, gains are taxed as ordinary income.

- Long-term gains: If you hold for more than one year, gains are taxed at the collectible rate — up to 28% — rather than the standard long-term capital gains rate.

- Net Investment Income Tax (NIIT): High-income earners may also owe an additional 3.8% NIIT on gold gains.

- Reporting: Sales of gold above certain thresholds require dealers to file 1099-B forms with the IRS.

The tax treatment of physical gold is noticeably less favorable than that of a Gold IRA, particularly for investors in higher income brackets.

Which Option Performs Better During Economic Uncertainty?

A Practical Investor Perspective

Many investors focus only on gold’s price performance, but ownership structure matters just as much. During periods of economic stress, both a Gold IRA and physical gold generally track the same underlying gold price. However, the investor experience can be very different.

For example, someone holding physical gold may have immediate access to their assets during a financial emergency. In contrast, Gold IRA investors benefit from tax advantages but must follow retirement account rules when accessing funds.

This distinction becomes particularly important during market downturns. Investors who prioritize flexibility often appreciate direct ownership, while those focused on long-term retirement planning may value the tax efficiency of a Gold IRA more than immediate accessibility.

Both Gold IRAs and physical gold are ultimately backed by the same underlying asset — gold itself. In terms of price performance during periods of economic stress, the metal behaves the same regardless of how you hold it. That said, the context matters.

Inflation

Gold has historically maintained purchasing power during inflationary periods. When the dollar weakens, gold priced in dollars tends to rise. From 2020 to 2022, U.S. inflation climbed to its highest levels in four decades, and gold held its value while many other assets suffered.

Recessions

During recessions, investors often flock to gold as a “safe haven.” This demand can push prices higher even as equities fall. In 2008–2009, gold rose more than 25% while the S&P 500 dropped roughly 50% from its peak.

Market Volatility

Gold’s low correlation with stocks makes it a natural portfolio stabilizer. Adding gold — whether through a Gold IRA or physical ownership — can reduce overall portfolio drawdowns during equity bear markets.

Currency Concerns

If you’re worried about the long-term value of the U.S. dollar or the global reserve currency system, physical gold in hand offers a level of independence from financial system institutions. For investors with deep concerns about systemic financial risks, direct physical ownership may feel more reassuring than gold held in any financial account.

Who Should Choose a Gold IRA?

A Gold IRA is likely the better fit if you:

- Are focused on retirement savings: You plan to hold gold for 10+ years and want the tax advantages of an IRA structure.

- Are in a higher tax bracket: Tax-deferred or tax-free growth offers the most benefit when your current marginal rate is high.

- Already have existing retirement accounts: A Gold IRA rollover from a 401(k) or traditional IRA lets you move funds without a tax event.

- Prefer institutional structure: You’d rather not deal with home storage logistics, insurance, or the emotional temptations of direct ownership.

- Want professional storage: You’re comfortable paying annual fees for the peace of mind that comes with a regulated depository.

Example: A 52-year-old professional with a $400,000 traditional IRA looking to diversify 10–15% into precious metals would be well-served by a Gold IRA rollover. The tax-deferred growth, professional storage, and structured withdrawal rules align well with retirement planning goals.

Who Should Choose Physical Gold?

Physical gold makes more sense if you:

- Want immediate access: You may need to liquidate quickly in an emergency and can’t afford to wait on IRA distribution processes.

- Value privacy and simplicity: You prefer to own gold without any institutional involvement.

- Are you investing outside of retirement? You’re buying gold as a general savings vehicle, not specifically for retirement.

- Have modest amounts to invest: Buying $5,000–$10,000 in gold coins doesn’t justify the overhead costs of a Gold IRA.

- Are concerned about systemic financial risks: You want gold that’s physically in your possession, not held by a third party.

Example: A 35-year-old with a fully funded emergency fund and maxed-out 401(k) who wants to keep $10,000 in gold as a hedge against inflation outside of retirement accounts is a natural candidate for physical gold coins stored in a home safe or private vault.

Can You Own Both?

Absolutely — and for many investors, owning both is the most balanced approach.

A Gold IRA covers your retirement-focused gold exposure with the benefit of tax-advantaged growth. Physical gold in a private vault or home safe provides liquidity, privacy, and emergency access that a Gold IRA can’t offer.

For example, an investor might allocate 70% of their gold holdings to a Gold IRA for long-term retirement purposes, and 30% to physical coins stored in a vault for short-term flexibility and peace of mind. This combination captures the tax efficiency of the IRA structure while maintaining the direct access and independence of physical ownership.

Diversification within gold — not just between gold and other assets — is a legitimate and practical strategy.

Frequently Asked Questions (FAQ)

Is a Gold IRA safer than owning physical gold?

Neither is inherently “safer” — the risks are just different. A Gold IRA stores your metals in a professionally secured, insured depository, eliminating the risk of home theft. But it introduces custodian risk and regulatory risk. Physical gold at home eliminates third-party institutional risk but exposes you to theft and the limits of personal security. Physical gold in a private vault is arguably the most secure storage method of all, though it comes with its own fees and counterparty considerations.

Can I keep Gold IRA metals at home?

No. IRS rules prohibit storing Gold IRA assets at home or in a bank safe deposit box. All metals must be held at an IRS-approved depository. Attempting to keep Gold IRA metals at home is considered a distribution, which triggers taxes and penalties.

What are the tax benefits of a Gold IRA?

A Traditional Gold IRA allows tax-deferred growth — meaning you won’t owe taxes on gains until you take distributions in retirement, typically when you may be in a lower tax bracket. A Roth Gold IRA allows completely tax-free growth and withdrawals, making it powerful for younger investors expecting higher future tax rates.

Is physical gold easier to sell?

In some ways, yes. You can sell physical gold to any local coin dealer or bullion dealer at any time — there’s no custodian process to go through. However, selling physical gold requires finding a buyer, negotiating a fair price, and handling the transaction yourself. A Gold IRA liquidation goes through your custodian, which adds a step but also ensures compliance with IRS reporting requirements.

What types of gold qualify for a Gold IRA?

The IRS requires gold to be at least .995 fine (99.5% pure). Qualifying items include American Gold Eagle coins (which are the only exception to the purity rule at .9167 fine), American Gold Buffalo coins, Canadian Maple Leaf coins, Austrian Philharmonic coins, and gold bars from COMEX or NYMEX-approved refiners. Collectible coins, graded coins, and jewelry are not allowed.

How much gold should be in a retirement portfolio?

Most financial advisors suggest keeping between 5% and 15% of a retirement portfolio in gold or other precious metals. This range is enough to provide meaningful inflation protection and diversification benefits without over-concentrating in a single commodity that produces no income. The right percentage depends on your overall asset allocation, risk tolerance, and proximity to retirement.

Are Gold IRA fees worth paying?

For most long-term retirement investors, yes. The annual fees — typically $200–$600 per year, depending on the custodian — are offset by the tax benefits of holding gold in a retirement account. If you’re in a high tax bracket and plan to hold gold for many years, the tax savings from deferred or eliminated capital gains taxes can significantly outweigh the fee costs. However, for small account balances or short holding periods, the fees may not be justified.

Can retirees own both a Gold IRA and physical gold?

Yes, absolutely. Owning both is common among retirees who want the tax advantages of an IRA for the bulk of their gold exposure, while maintaining direct access to a portion of their physical gold for emergency liquidity. There are no rules prohibiting someone from holding a Gold IRA and separately owning physical gold coins or bars outside of any retirement account.

Common Mistakes Investors Make When Choosing Between a Gold IRA and Physical Gold

After reviewing the advantages and limitations of both options, several mistakes appear repeatedly among first-time gold investors.

Focusing Only on Tax Benefits

Some investors choose a Gold IRA solely because of its tax advantages without considering annual fees and withdrawal restrictions. Tax benefits are valuable, but they should not be the only deciding factor.

Ignoring Storage Costs

Physical gold ownership provides direct control, but secure storage is not free. Investors often underestimate the cost of safes, insurance, or professional vault services.

Overallocating to Gold

Gold can be an effective diversification tool, but concentrating too much wealth in a single asset may increase portfolio risk. Most financial professionals view gold as one component of a broader investment strategy rather than a complete retirement solution.

Choosing Based on Fear

Gold frequently attracts attention during periods of economic uncertainty. While caution is understandable, investment decisions should be based on long-term goals rather than short-term headlines or market fears.

Final Verdict: Gold IRA vs Physical Gold

When comparing Gold IRA vs Physical Gold, the better choice depends less on the metal itself and more on how you intend to use it within your overall financial plan.

A Gold IRA is generally better suited for investors focused on retirement savings, tax efficiency, and long-term portfolio diversification. The structured environment, professional storage, and potential tax advantages can make it an attractive option for individuals building wealth over decades.

Physical gold, on the other hand, appeals to investors who value direct ownership, immediate access, and greater control over their assets. It can serve as a useful complement to traditional investments and may provide additional peace of mind for those who prefer tangible assets.

For many investors, the most balanced solution is not choosing one over the other but combining both approaches. A Gold IRA can support long-term retirement goals, while a modest allocation to physical gold can provide flexibility and personal control outside retirement accounts.

Ultimately, the best strategy is the one that aligns with your financial objectives, risk tolerance, and time horizon. Before investing, consider consulting a qualified financial advisor or tax professional to ensure your gold allocation supports your broader wealth preservation plan.

Disclaimer:

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a licensed financial professional before making investment decisions.